1 min read

The 2014-2015 winter harvest season has come to an end in the Lake States region. Now that I have had a few days to catch my breath, I have been thinking about many of the industry-specific conversations that I was involved in over the long winter months and I want to take this opportunity to briefly share my takeaways about the Lake States timber market.

- The 2014-2015 winter harvest season was better than last winter’s season. Since system inventory levels were lower than planned as we entered winter 2014-2015, however, some mills are still facing critical inventory issues.

- Inventory levels have not yet fully recovered. Currently, they average roughly 75-80% of capacity and this shortage is likely to extend through the spring season.

- Pulpwood pricing during Q1 was very competitive and I believe this trend will continue through the summer months. This resulted in higher pricing for nearly all species, and I expect this premise to be confirmed through Forest2Market’s Q1 benchmark data.

- Suppliers were able to capitalize on a seller’s market. Some are of the opinion that retirement-aged suppliers may opt to ride out the seller’s market, postponing retirement until the market turns at which point they will sell their equipment and head for greener pastures.

- Despite the fact that the harvest season was better this year, logging and trucking capacity was still insufficient to meet mill requirements. For certain industry cynics, this substantiated the fact that a logging/trucking capacity issue does in fact exist.

- Some suppliers—in contrast to others taking advantage of the seller’s market to build their nest eggs—are beginning to make investments in new equipment, something they have been avoiding in the wake of the recession.

- While cut-to-length (CTL) harvesting systems can operate on heavier soils, logging road infrastructure has deteriorated. This reduction in road quality is limiting or restricting altogether the capacity to move wood from stump to mill.

We’re still waiting on the remainder of the Q1 Lake States data to be aggregated into our delivered raw material cost database, at which time we will offer additional observations about volume and price in the upcoming newsletter.

2019 FAO Report Highlights State of Global Forest Markets

The 2019 edition of the United Nations Economic Commission for Europe (UNECE) and the Food and Agriculture Organization of the United Nations (FAO) ...

Australia’s Forest Products Industry Continues to Grow in 2017

Per a new report from Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES), the Australian forestry sector continued to...

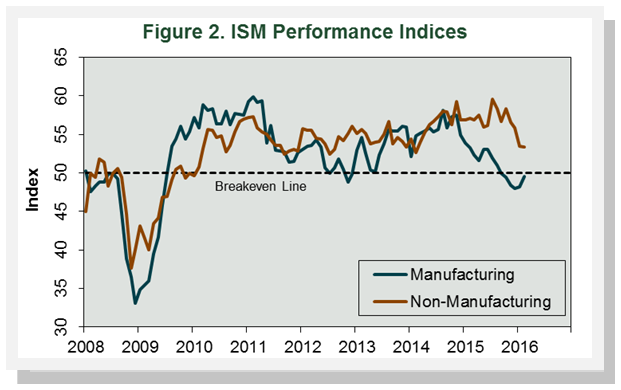

Forest Industry Performance: February 2016

Forest industry performance in January and February was reported by both the US government and the Institute for Supply Management.