Suz-Anne Kinney

Suz-Anne Kinney

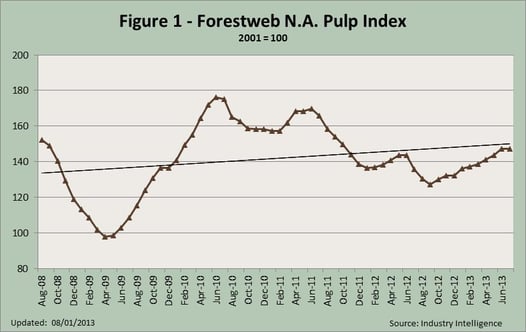

In June and July of 2013, the Forestweb N.A. Pulp Index approached it’s 5-year trend line for the first time since November 2011. Since hitting a 2012 low in September, the index has shown improvement, gaining 16 percent through July 2013 (nearly at the same level of February 2012). Currently, the index reads 147.38, higher than both the average (142.94) and the median (143.54) between 2007 and 2013 YTD.

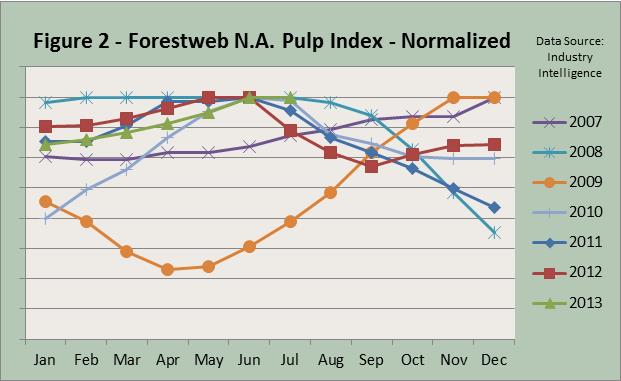

In our May 31, 2013 post, Pulp Prices: Have We Hit the 2013 High?, we speculated we would see the market high in either May or June, primarily because of the following chart, which normalizes the Forestweb index by pegging the yearly high at 100 percent and all other prices as a percentage of that high. This chart shows that for each year since 2010, the market high for the year occurred in either May or June. When we add the 2013 data, we see that prices are gently bucking the trend. The index did reach a high (YTD) in June, but then it repeated that level in July. By doing so, the index appears to be following the 2010 trend, as prices fell only slightly in July after a June high.

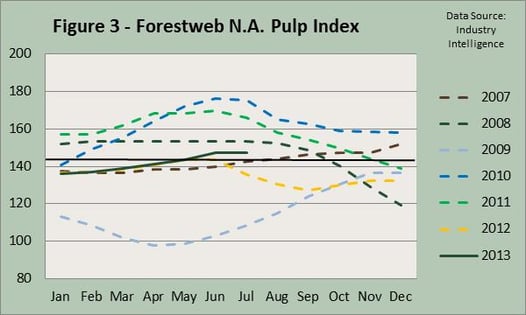

Long term, however, if the past is prologue, chances that prices will continue to climb and actually breach the five-year trendline seems unlikely. Figure 3 shows the (non-normalized) trends since 2007. Prices ended the year higher than they they were in the May-June timeframe in just two of these years (2007 and 2009).

There have been no announcements for price increases for August. According to Diane Keaton of Industry Intelligence, industry participants are generally expecting the market to soften, primarily because growth in China is slowing. Though demand in the US remains strong (FOEX reports that demand for NBSK in the first half of the year was up 7.7% over 1H2012), the pulp market is global; when China’s economy slows, pulp prices feel the effect worldwide. As a result, we expect prices to decrease in 3Q2013.

Pulp Prices: Have We Hit the 2013 High?

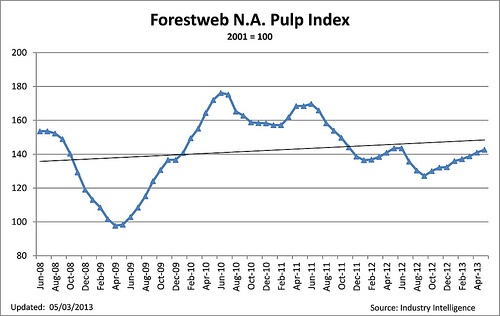

Where are pulp prices, and where are they headed? According to the Forestweb North American Pulp Index, which is published by Industry Intelligence,...

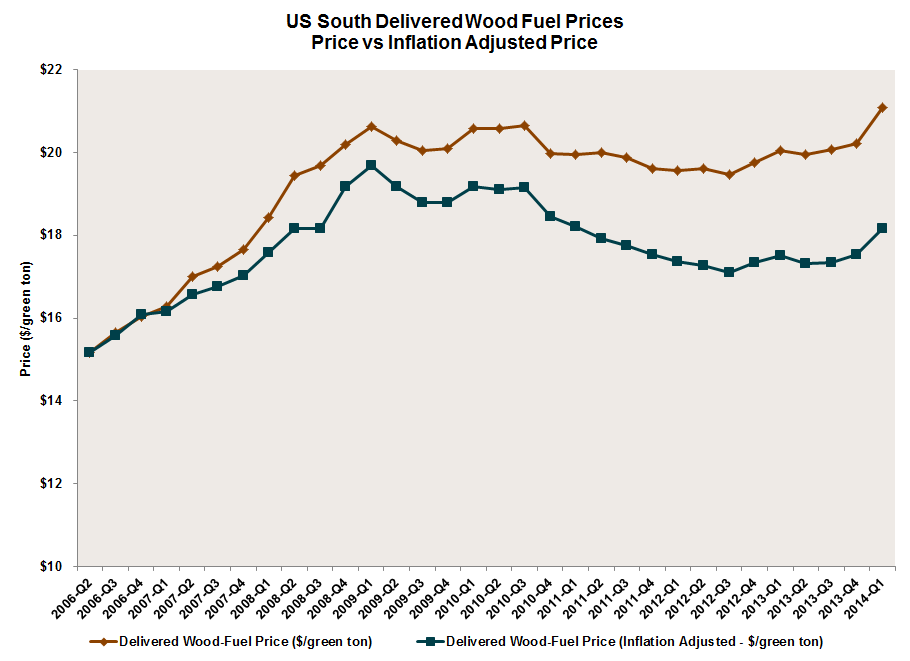

Wood Fuel Prices in US South - 1Q2014

Wood fuel delivered prices in the first quarter of 2014 increased $1.04 per ton, or 5.2 percent, from the first quarter 2013 average price of $20.05...

Timber Price Movements in the US South during March/April 2016

Timber price trends during the March/April 2016 period saw pulpwood prices decreasing and sawtimber prices remaining relatively flat. Pine pulpwood...