With so much activity that has occurred in the pulp and paper industry over the last quarter, it’s difficult to keep up with some of the major developments that could impact various segments across the industry. To provide a high-level snapshot of some of these major industry moves, we’ve rounded up some of the leading headlines below.

Stora Enso’s Multiple Divestments and the Future of the Langerbrugge Site

At the end of March 2022, Stora Enso announced its plan to divest four of its five paper sites in order to focus on strategic growth areas. The paper production sites included in the divestment are Anjala in Finland, Hylte and Nymӧlla in Sweden, and Maxau in Germany.

“Through divesting a majority of our paper assets, we are able to increase the focus on our defined strategic growth areas of renewable packaging, building solutions and biomaterials innovations. When assessing potential divestment options, we look for new ownership that will provide a sustainable longer-term future for the sites and the people that work there,” said President and CEO Annica Bresky.

But what will happen to the one mill excluded from the divestment?

At the beginning of June, Stora Enso disclosed its intentions for the remaining Langerbrugge site in Belgium – to rebuild the newsprint machine to produce recycled corrugated case material. The company is currently in the process of a feasibility study at this site for the conversion process, which is expected to be finalized in the first half of 2023.

Assuming everything goes as intended, the converted line is expected to be in production by 2025 and will produce an annual capacity of 700,000 tonnes of testliner and recycled fluting grades – generating annual sales of EUR 350 million when running at full capacity. This conversion would enable Stora Enso to further grow its recycled and recyclable packaging materials capacity and meet the growing demand in end-use segments such as e-commerce.

"Today we produce recycled containerboard in Poland, mainly for the Eastern European market. A conversion in Langerbrugge would establish a competitive position for us in Western Europe as well," explained Hannu Kasurinen, Executive Vice President, Packaging Materials division. "In addition to sourcing materials for recycled containerboard, the study will also assess the handling of different incoming recycling streams, including laminated grades.”

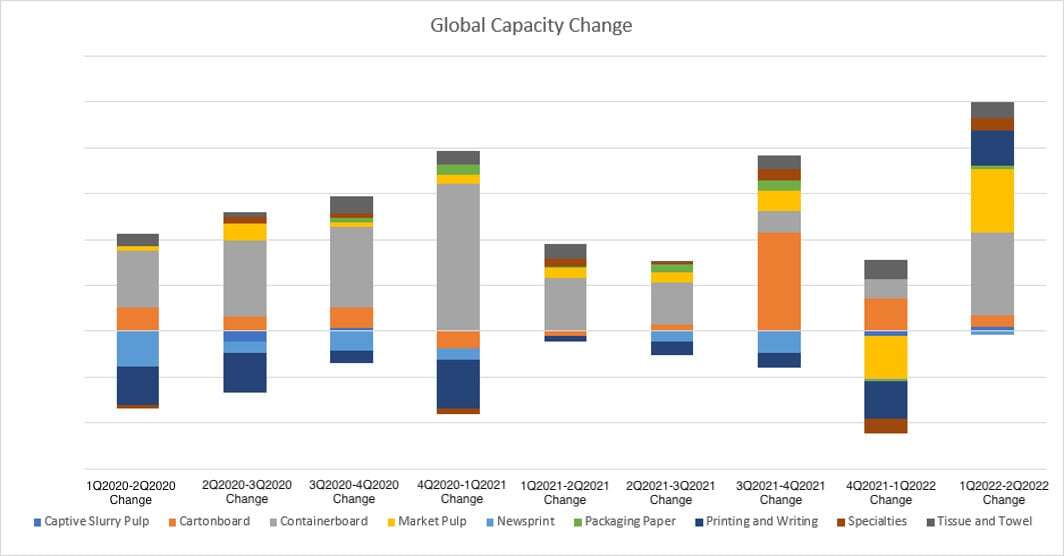

2Q Experiences the Most Added Capacity in the Last 10 Quarters

2Q2022 saw the most tons of capacity added in the last 10 quarters. As we can see from the image below, cartonboard, containerboard and market pulp were the primary contributors – which doesn’t come as a surprise given the strong demand in these segments.

Source: FisherSolve

Source: FisherSolve

Current and announced containerboard capacity continues to grow with each passing quarter – largely due to the bustling e-commerce segment that has fueled the need for more shipping boxes. As a result, companies such as WestRock, Pratt Industries, International Paper, Kruger, and many more are investing in expanding domestic corrugated capacity through new boxplants in order to keep up with new demand. The containerboard segment is expected to reach some of the highest numbers at the end of 2022 with more than 43,700,000 TPY of total capacity in the US.

While market pulp demand drove prices exponentially higher in 1H2021, current prices and demand haven’t dropped too much from 2021 levels. Due to factors such as supply chain issues, challenges in the recovered paper markets, and the war in Ukraine, many manufacturers were forced to move production closer to the customers they service in order to meet the demand that was much greater than initially predicted at the end of 2021.

HEINZEL GROUP’s Acquisition of UPM’s Steyrermühl Mill

On June 21, 2022, HEINZEL GROUP announced its share purchase agreement with UPM to acquire UPM Kymmene Austria GmbH and its subsidiaries in Steyrermühl, Upper Austria. The goal for this acquisition is to transform Heinzel’s Laakirchen Papier AG and UPM’s Steyrermühl mill, which are less than three kilometers from each other, into a hub for sustainable packaging papers and renewable energy once the transaction is closed on January 1, 2024.

UPM plans to continue current operations of its lone paper machine for newsprint production, and sawmill and residue incineration plant co-owned with Heinzel’s Laakirchen Papier until the end of 2023 when it will cease the production of graphic papers.

HEINZEL GROUP produces a range of papers for flexible packing, or kraft papers, and rigid packaging, or containerboard, at its various sites. This new acquisition will help complement its existing products as it looks to grow in the sustainable packaging papers segment. HEINZEL GROUP is also heavily considering developing Steyrermühl into a supply center for heat and energy for both the Laakirchen paper mill and the wider Laakirchen community.

Fisher International can provide you with a deeper analysis into these industry developments and how they might impact your business and influence your decision-making. Our consulting services help provide you with answers to important questions by explaining market movements in verifiable, fact-based and common-sense terms that industry professionals find useful. To learn more about how Fisher’s consulting team can help you prepare for new opportunities, contact us today.

Unsaturated Polyester Resin Outlook 2026: Weak Demand and Uneven Regional Pricing

Polyamide Markets at Mid-Year 2026: Cost Pressure, Weak Demand and European Restructuring

Major Moves in the P&P Industry that Occurred in 3Q 2022

With so much activity that has occurred in the pulp and paper industry over the last quarter, it’s difficult to keep up with some of the major...

The P&P Industry Kicks Off October With Impressive Sustainability Developments

Each month, we continue to see the innovative concepts companies are developing in order to pursue a greener economy. The Pulp and Paper industry has...

How Fisher International Predicted the Recyclability of Fiber-Based Packaging

In 2017, Fisher International presented at TAPPI’s Papercon on the state of recycled fibers. At the time, our modeling suggested that the “seven...