Hira Saeed

Hira Saeed

What the UCO Market Reveals About Crude Tall Oil Demand

What's Next for Asia's Largest Wood Pellet Supplier?

How Plunging PVC Demand is Behind the Recovery in the Caustic Soda Market

As the world battles to control the Covid-19 outbreak, demand in many chemical sectors is tumbling. With automotive and construction industries...

1 min read

How is COVID-19 Impacting the Caustic Soda Market Around the World?

Since the COVID-19 virus hit Europe in January, infection cases have been rising and while initially there was no immediate impact on the market,...

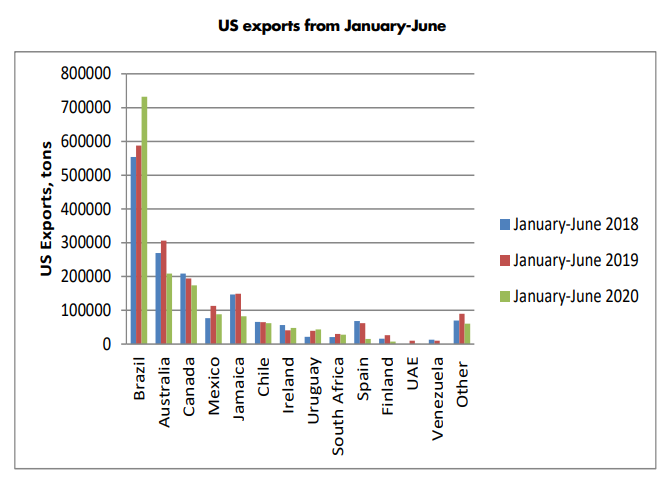

Post-Covid-19 Changes in Caustic Soda Trade Flows in the US

Before the COVID-19 outbreak, demand for caustic soda was firm, with most sectors showing steady growth over the past few years. However, when the...