Javier Rivera

Javier Rivera

The Pulp Mill as a Biorefinery: Unlocking New Revenue Streams

Bio-Bunker Premiums Rebound as Oil Market Disruption Eases

Is the US Automotive Sector Strike Impacting Chemicals Supply Chains?

The automotive sector is operating in a contradictory landscape at present. This year alone, it has been subject to pent-up demand driven by Covid,...

1 min read

Engineering Thermoplastics: Calming Markets or More Chaos Ahead?

After the tumultuous start to 2021, engineering thermoplastics market participants were expecting a return to more representative activity starting...

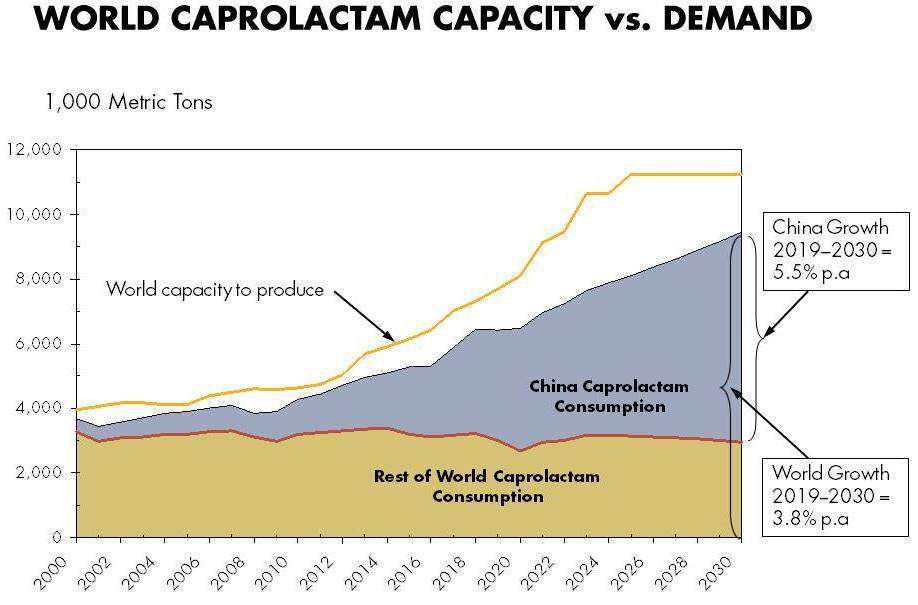

China’s Caprolactam, Adiponitrile Markets Face Opposing Forces

The outlook for polyamide market demand, the stop-and-start nature of economic recovery during the COVID pandemic, and key feedstock materials – both...