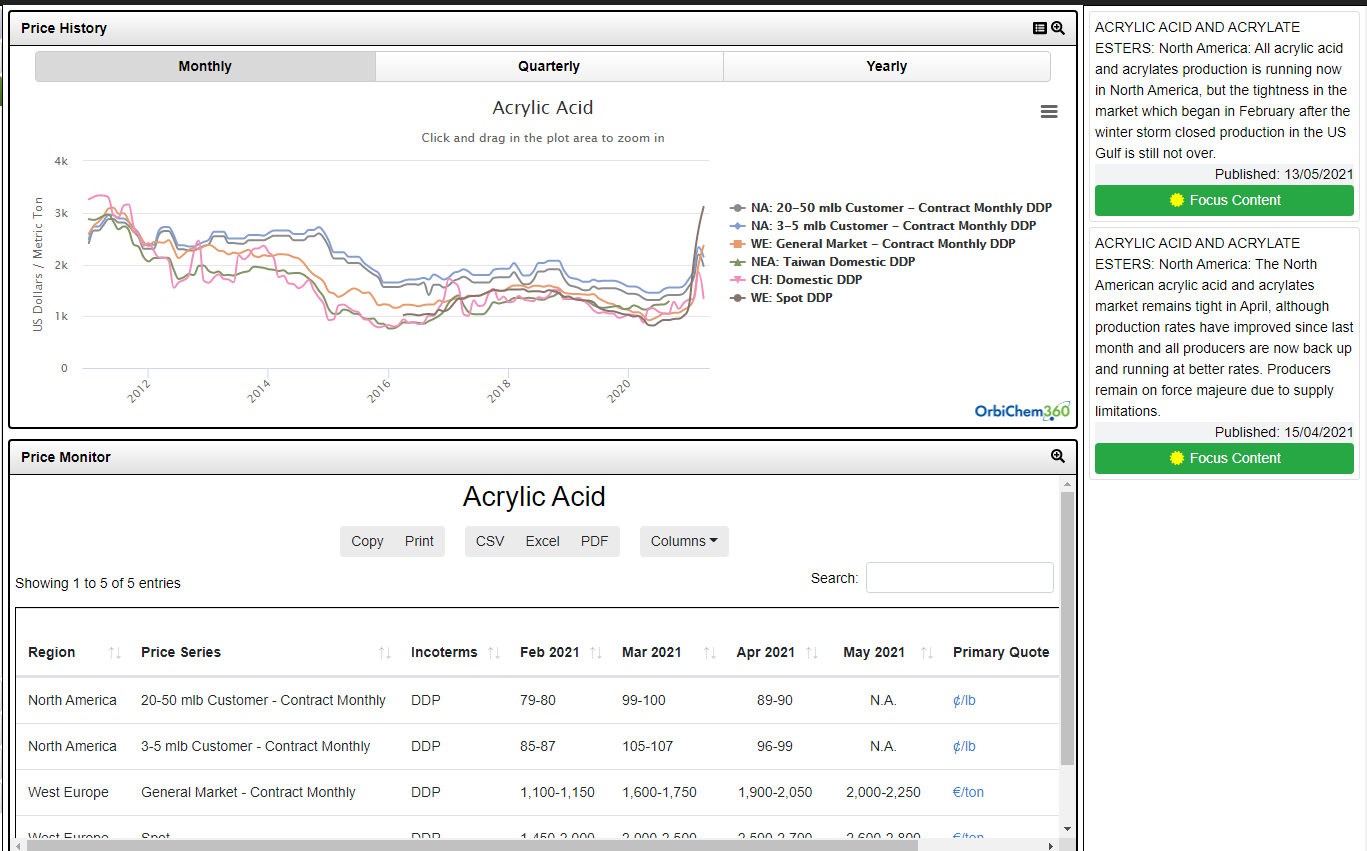

To say this year has proved a huge challenge for the acrylic acid and acrylates market would be a vast understatement. Buyers have faced a huge mountain to climb to secure material and ensure downstream operations can run to the best degree possible, in some cases facing lengthening lead times and delivery delays.

The shifting pattern of demand brought about by the COVID-19 pandemic and its after-effects has led to an unpredictable market situation. Global supply chain disruption has magnified the tight situation in many countries.

A series of production issues, tight feedstock supply, and industry-wide inventory depletion has led to the current situation. The exacerbating factor, however, has been the soaring freight rates which have deterred imports of critical products from Asia due to tight vessel space, making the costs extremely high.

The first product to undergo a radical change in direction was butyl acrylate, with the supply issues in the European market being the catalyst for a global shortage. Severe and lasting production limitations at BASF’s Ludwigshafen BA plant coincided with the long-term closure of Dow’s Boehlen Germany BA plant last year. A series of further production issues have followed globally, culminating in the big freeze in the US Gulf Coast which pushed the North American GAA and acrylates market to an unprecedented state of tightness, as one by one all producers declared force majeure. An extremely tight oxo-alcohols were also a limiting factor to BA and 2-EHA production. Prices have increased enormously in all regions over the past 6 months as acrylic acid and acrylates shifted rapidly from a buyers' to a sellers’ market.

Rachel Uctas

Rachel Uctas