Jane Denny

Jane Denny

Epoxy resin producers in Europe and the US met with concerned buyers and increased inquiries as 2024 began.

Despite the price point for epoxy resins from the Asia region being considerably lower than North America and Europe—Panama and Suez Canal disruptions put paid to deals between western buyers and Asian producers.

Delayed shipments and rising freight costs created a flurry of activity and price increases in Europe. However, the year closed with both the US and European markets in limbo. Anti-dumping investigations in Europe and the US created uncertainty among buyers.

Asian producers, meanwhile, faced oversupply and underperforming markets—fundamentals that have carried through to 2025.

ResourceWise Business Manager Jennifer Hawkins shares her thoughts on what the remainder of 2025 will bring.

Epoxy Resin in Focus

Soon after 2024 began, low stock levels were seen across the entire epoxy resins value chain. This came alongside reduced run rates at most plants, and as global shipping disruptions continued, benzene values rose. In this scenario, epoxy resin prices were pushed slightly upwards.

As supply chains remained unsettled, buyers became uncertain, prompting them to pre-buy ahead of a strong uptrend in raw materials. This mix of fundamentals continued to pull buyers back into their domestic markets. For example, European spot business picked up as delayed imports left customers feeling vulnerable.

By March, the US epoxy resins market was pulled in different directions due to opposing forces. Faltering consumer confidence and ample supply pushed prices down. The hikes in feedstock costs and freight rates—amidst security of supply concerns—had pushed buyers back into the domestic market. Producers sought further price increases and began to consider that recovery was in play. There was bullishness in the US epoxy resin value chain, particularly BPA, as Q1 drew to a close and Q2 began.

April saw a seasonal pick-up in epoxy resin demand in the US, but offtake volumes remained up to 30 percent lower than pre-Covid, said downstream consumers. European suppliers felt the need to regain ground lost due to feedstock cost increases.

Trade Protectionism Sweeps Epoxy Resin Markets

Just as US seasonal demand for epoxy resins swung into play in April, the country’s Department of Commerce and the US International Trade Commission announced an anti-dumping investigation on imports from key Asian competitors. The complaint was spearheaded by US-headquartered chemical manufacturing co-complainants Olin and Westlake.

White Paper Download

Download ResourseWise Chemicals Business Manager Jennifer Hawkins' analysis of EU

and US ADD investigations and International Trade Commission conference submissions, including insight from her epoxy resin market contacts.

The antidumping duty (AD) investigation was initiated for epoxy resins imported by the US from China, India, Korea, Taiwan, and Thailand. It also included countervailing duty (CVD) investigations of epoxy resins from China, India, Korea, and Taiwan.

The anti-dumping investigation prompted bullish behavior by US producers at the mid-year point. They pushed hard for price increases, leaving little room for buyer resistance. The backdrop to this was a lackluster US bisphenol A market. There was no real pickup in demand from epoxy resin production, and polycarbonate demand remained muted.

European Commission Anti-dumping Probe

Within a few months, the Ad Hoc Coalition of Union Epoxy Resin producers (Olin, Westlake Epoxy and Spolchemie) complained of Asian uncompetitive practice producers to the European Commission (EC).

The submission triggered investigations into the trading practices of producers in China, South Korea, Taiwan, and Thailand. In the midst of this, India's Ministry of Commerce initiated an AD investigation into liquid epoxy resin imports from complainants, as well as Saudi Arabia.

With output volumes up to 30 percent lower than pre-2019 levels globally, Olin, Westlake, and Spolchemie's move was a bid to stop cheap imports driven by huge expansions and dwindling markets in Asia. It is highly likely that anti-dumping investigations muted foreign trade deals for epoxy resins to some extent.

The EC published its pre-disclosure summary of proposed provisional duties at the end of January 2025. According to the summary, Chinese companies will face ADD of up to 40.8 percent, Taiwan could face up to 11 percent, and Thailand 32.1 percent. South Korea will not face any anti-dumping levies. Provisional measures were published on 27 February, with rates remaining unchanged. A two-week window for companies to respond to the findings followed.

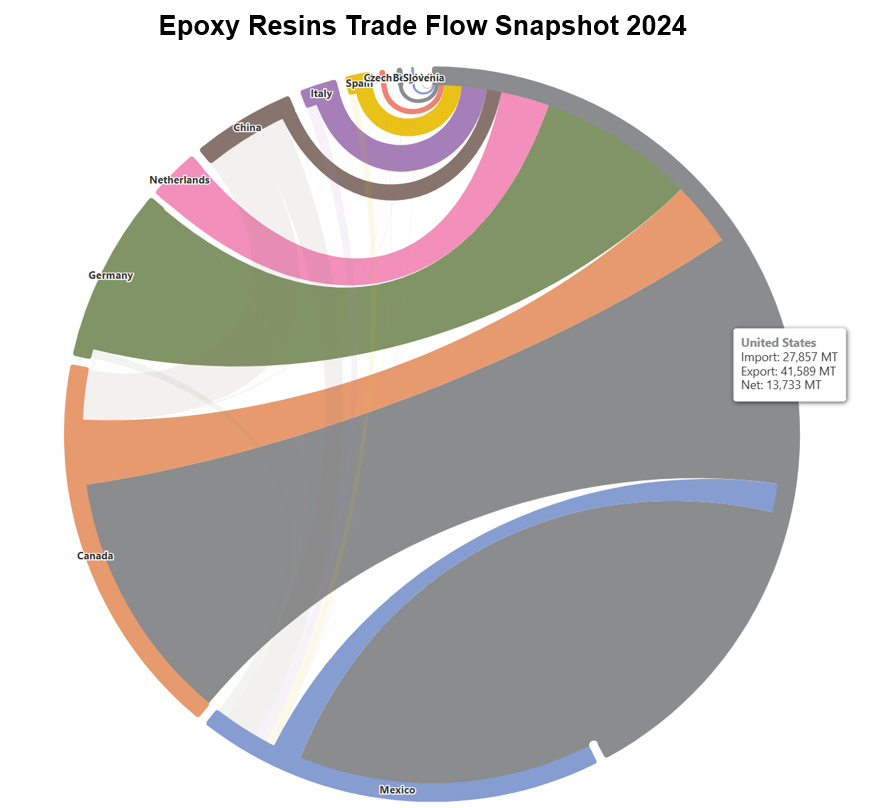

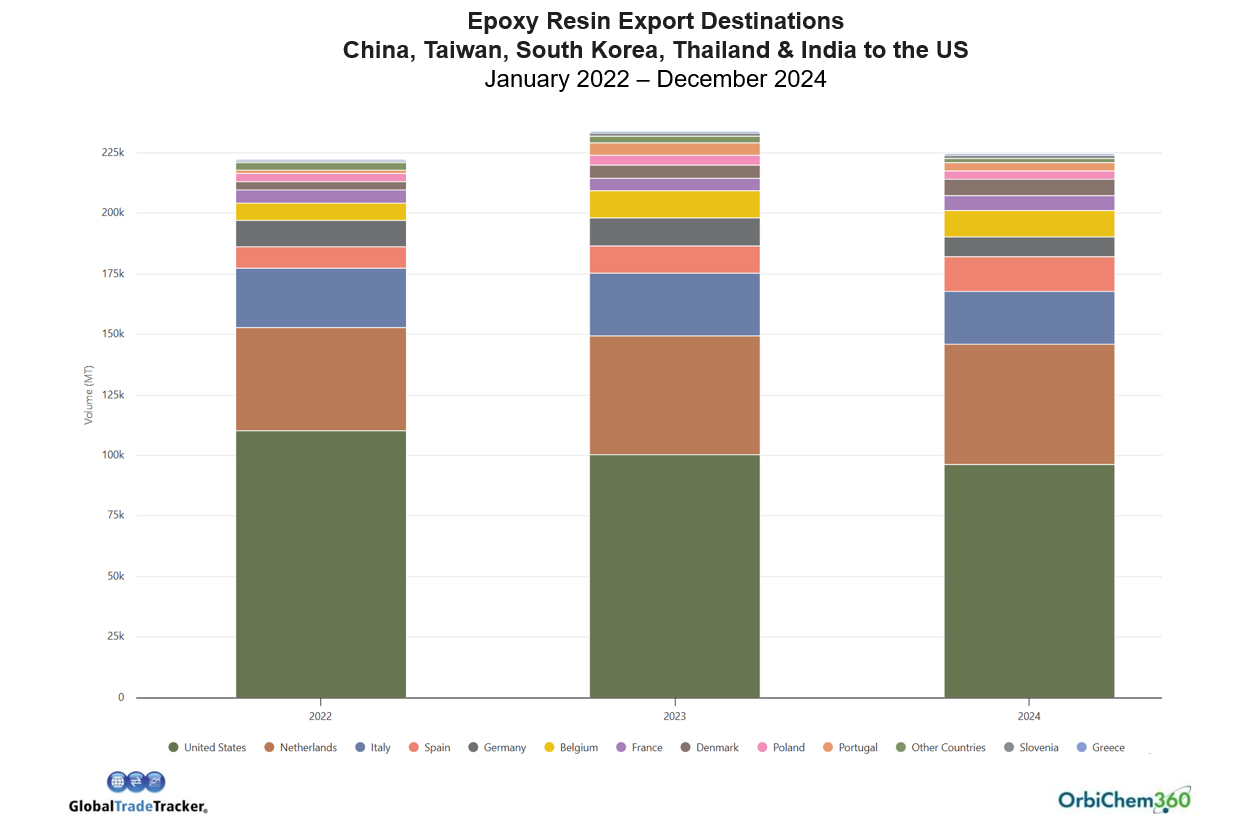

US Epoxy Resin Imports

According to the ResourceWise chemical intelligence platform OrbiChem360, in the five-year period between 2015 and 2019, an average of around 72 ktpa of epoxy resin was collectively shipped from the five key exporting countries at the heart of AD measures and probes—namely China, India, Korea, Taiwan, and Thailand.

That figure rose to an average in excess of 100 ktpa from 2022 to November 2024.

Exports from China, Taiwan, South Korea, Thailand, and India to the US between 2015 and 2020 were well under 80 ktpa. Indeed, they were much lower—especially in 2020 due to COVID-19.

However, since 2020, the volume of epoxy resins imported into US markets from those partner countries has grown to an average of over 100 ktpa. The graph below (click the image to see the graph on a new page) shows trade between the US and countries accused of dumping.

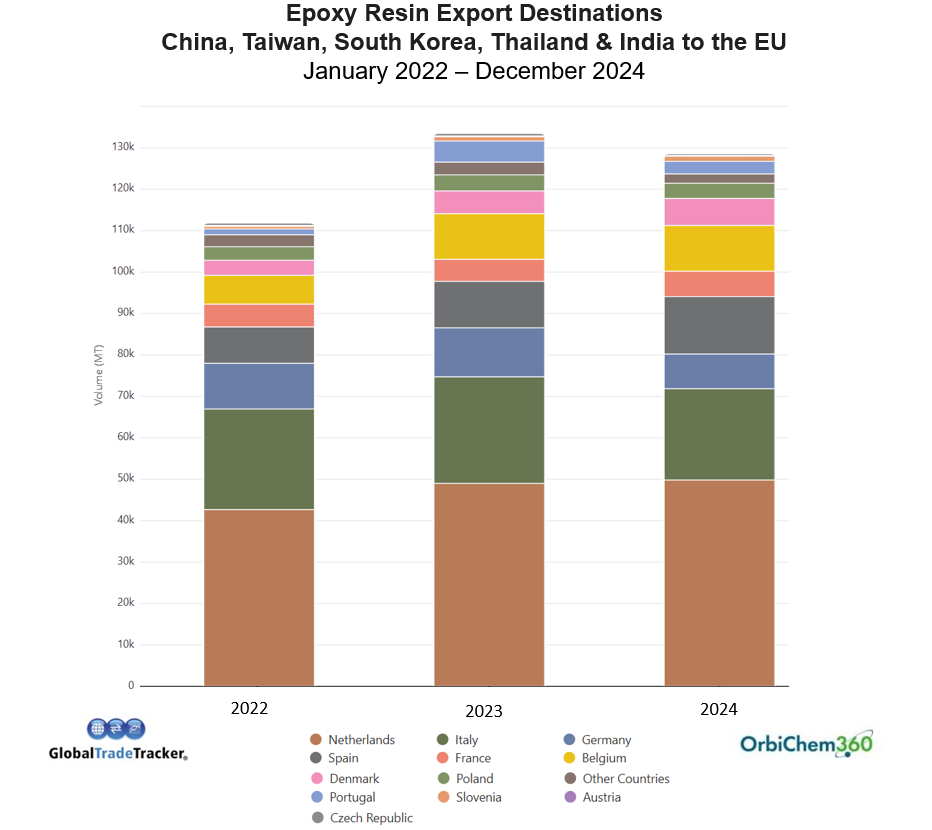

EU Epoxy Resin Trade: A Snapshot

The graph below (click image to open in a new page) shows that imports to the European Union by product dumping suspects in 2023 were significantly higher than in the prior year, then dropped lower in 2024, possibly due to the EC's investigation.

Bisphenol A

Asian bisphenol A (BPA) producers started 2024 with negative margins and a waning US buyer base. Erstwhile western buyers turned to domestic markets as maritime logistical issues hampered deliveries and drove freight rates upwards.

Chinese BPA prices briefly rose to a seven-month high in July due to low operating rates and increasing feedstock phenol prices. They quickly fell again due to ample availability, as shown in the graph above.

Suppliers had hoped there would be a pick-up in BPA demand in the US, but the market remained lackluster with very few enquiries for spot material.

As the year drew to a close, markets in all regions stayed quiet due to the usual year-end seasonal slowdown.

Epichlorohydrin

By April, the general feeling was that epichlorohydrin markets could not worsen, although European suppliers felt the need to regain ground lost due to feedstock cost increases. The product’s availability meant prices moved in line with feedstock costs only. Imported epichlorohydrin prices were such that domestic suppliers were unable to compete.

Chinese epichlorohydrin prices rose from floor levels after falling to a 10-month low in June 2024. However, demand remained weak. Spot activity in the US and European markets picked up as buyers sought to mitigate the impact of delayed deliveries.

Domestic Chinese epichlorohydrin values decreased in Q3 due to weak demand but rose in mid-November due to production shutdowns. As the year closed, Chinese prices dropped, and several producers restarted as a new plant came onstream.

While the US experienced better-than-expected epoxy resin demand as the year began—which boosted epichlorohydrin offtake volumes—the market remained very quiet as 2025 approached.

Looking Ahead: 2025

With ADDs in both regions essentially closing the door to Chinese imports, Asian suppliers have been given the impetus to push for price increases.

In Europe, ADDs could impact 70,000 tons of imported epoxy resins from China, Taiwan, and Thailand (these were total volumes from January to December 2024). EU producers are hoping to recapture this market share and, by doing so, will continue to push for price increases in a bid to improve margins, which have been close to or below production cost levels for almost two years.

South Korean suppliers are also raising prices now that Chinese competition is been eradicated from Europe.

In the US, overwhelming uncertainty—first from the ADD investigation during 2024 and then the looming threat of tariffs on Mexican and Canadian imports—has driven buyers back into their domestic markets. Producers are succeeding in getting price hikes accepted. Markets are expected to remain on an uptrend until at least the first half of 2025.

Stay updated with chemical markets by subscribing to our newsletter or exploring our latest commodity reports.

What the UCO Market Reveals About Crude Tall Oil Demand

What's Next for Asia's Largest Wood Pellet Supplier?

ResourceWise's 2024 Forest Products Industry Predictions

In 2023, the pulp, paper, and forest industries navigated through a series of dynamic market shifts and unanticipated challenges. From fluctuations...

Chlor-alkali and PVC: 2025 Review and 2026 Outlook

The chloralkali and PVC industries ended 2025 facing another year defined more by structural adjustment than short-term volatility. Global...

Maleic Anhydride Markets: Review 2024 and 2025 Outlook

Demand for maleic anhydride from downstream sectors—including automotive, construction, and electronics, as well as the crucial unsaturated polyester...